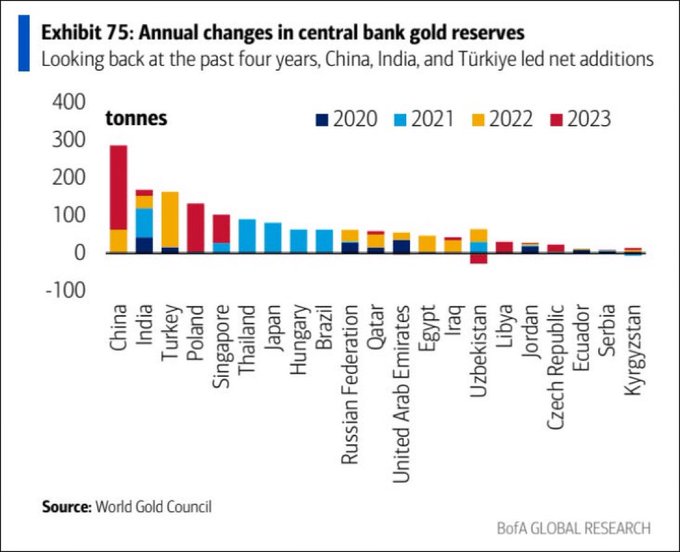

More precisely, the People’s Bank of China purchased gold for its reserves for a 17th straight month in March, while last month Bullion held by the People’s Bank of China rose by about 390,000 troy ounces. That takes total holdings to 72.58 million troy ounces, equivalent to about 2,257 tons, which is China’s central bank’s largest annual purchase in 2023 since 1977.

Click here to access our Economic Calendar

So far in April, the gold price has continued to set new record highs and briefly touched a high of $2365 per ounce. Confidence in the Fed’s easing cycle may have eroded somewhat, but safe haven demand and central bank buying have continued to keep prices underpinned.

Central Banks policy

The Fed has long warned that the cooling in inflation will not be on a linear path and the report reflected the stubbornness of price pressures. And while energy and housing contributed over half of the strength, there were modest gains in many other components, suggesting a broadening. Indeed, Powell’s “supercore” rate which also takes out housing, rose 0.65% on the month, after gains of 0.47% in February and 0.85% in January, according to Bloomberg.

According to The Kobeissi Letter, this significant rise in central bank gold acquisitions since early 2022 which continues to strongly support Gold reaching new highs, is a diversification strategy from Central banks in response to global economic pressures.

Central bank purchases exert a stronger influence on the gold market worldwide, as demonstrated by the consistent high demand seen over the past three years.

What are the driving factors? Why does gold price ignore Central Banks’ potential easing? Why are market correlations weak in Q2?

Looking ahead, the prospect of lower US interest rates, sustained Chinese demand, and geopolitical uncertainties are expected to continue bolstering gold prices. Immediate Resistance levels for gold remain at latest record high, at $2,365 barrier, while a break above that level could attract more bulls into the market towards the psychological threshold of $2,500 which represents the 161.8% Fibonacci extension level of the August 2023 rebound.

Particularly in China, the increase of gold reserves at unprecedented rates, is an attempt to lessen reliance on the US Dollar and the US debt crisis, to face economic challenges, particularly in the property market.

This surge in gold purchasing is partly attributed to reduced confidence in immediate interest rate cuts from Central banks, positioning gold as an investment for stability and a potential hedge against inflation.

The gold’s unprecedented surge can be attributed to various factors, with central bank policies, geopolitical tensions, Chinese demand, and inflation hedging strategies playing significant roles.

In the long term meanwhile, Bank of America predicts that gold prices could hit $3,000 by 2025, citing the continuation of its record-breaking rally fueled by speculative trading. Additionally, Citi has raised its upper price targets for the next 6 to 12 months, setting them at $3,000 per ounce for gold as well and $32 per ounce for silver.